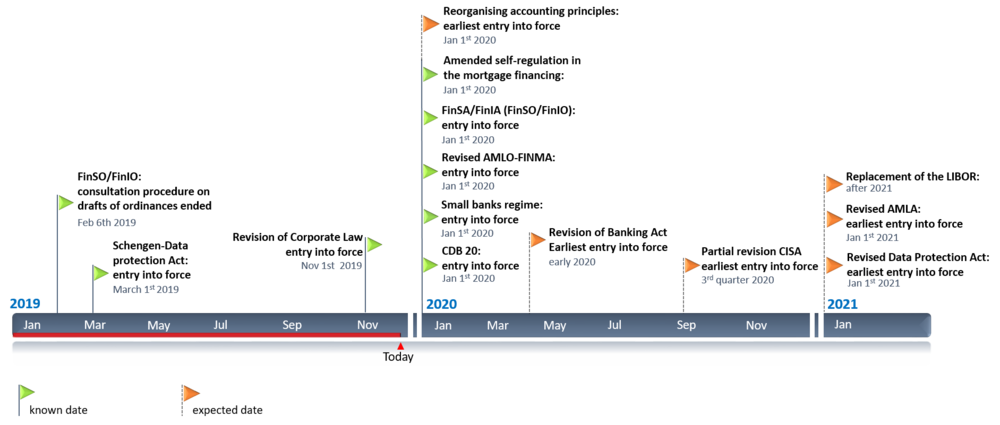

Review and Outlook

As of November 2019, the Federal Council enacted the Federal Act on the Implementation of Recommendations of the Global Forum on Transparency and Exchange of Information for Tax Purposes. The main changes relate to the conversion of bearer shares into registered shares for companies without stock exchange listing and companies whose shares have not been issued as intermediated securities. Such bearer shares must be converted within 18 months of the entry into force of the new federal law. This corresponds to a de facto abolition of bearer shares.

The dispatch on the revision of the Banking Act is expected to be published in spring 2020. As a result, the renewals will affect in particular the depositor protection of institutions in the event of bankruptcy and the way in which deposits are financed. There are also plans to amend the Collective Investment Schemes Act (CISA) to create a new fund category - a so-called Limited Qualified Investor Fund (L-QIF).

Following the pilot phase of the small banks regime in July 2018, the requirements for banks in Supervisory Categories 4 and 5 will be simplified by adjustments to the Capital Adequacy Ordinance and various FINMA circulars. In line with the principle of proportionality, the value adjustments for default risks will also be disclosed: only system-relevant banks will have to model the expected losses in their loan portfolios in detail; for banks in other Supervisory Categories, a principle-oriented procedure will suffice.

On 26 June 2019, the dispatch on the amendment of the Anti-Money Laundering Act (AMLA) was adopted. The planned amendments to the AMLA mainly address the weakness identified by the Financial Action Task Force. It is planned to introduce due diligence requirements for certain services in connection with companies and trusts, in particular in the areas of incorporation, management and administration. The revised Agreement to the Swiss Banks' Code of Conduct on Due Diligence (CDB 20) was also issued by the Swiss Bankers Association and will enter into force simultaneously with the new FINMA Anti Money Laundering Ordinance (AMLO-FINMA) on 1 January 2020.

Following the entry into force of FinSA and FinSO on 1 January 2020, it will be advisable to implement the rules of conduct of financial intermediaries to their clients. Furthermore, the FinIA and FinIO will enter into force simultaneously on 1 January 2020, standardising the licensing rules for asset managers, collective asset managers, fund management companies and investment firms.

The Fintech sector is also developing rapidly. On one hand, FINMA approached audit firms and some of the institutions concerned at the beginning of 2019 in a letter and, for the first time, issued an opinion on the accounting treatment and the resulting supervisory requirements in connection with payment tokens. On the other hand, the Federal Council dealt with the necessary adjustments to the Swiss legal framework in order to create the legal framework for blockchain and distributed ledger technologies - e.g. Securities Law, Debt Enforcement and Bankruptcy (“DEBA"), Banking Act (“BA"), Financial Market Infrastructure Act (“FMIA") and Anti-Money Laundering Act (AMLA).

The subject of data protection also remains topical: Less than a year after the General Data Protection Regulation (GDPR) came into force, Swiss financial service providers have dealt with the main features of the matter. In response to the needs of legislation in these areas, Switzerland published the Schengen Data Protection Act for the first time on 1 March 2019 and is now debating the totally revised Data Protection Act in its winter session. The entry into force of this totally revised law remains unclear. The issue of LIBOR also remains unclear: the British FCA has announced that it will no longer force the panel banks to participate in the LIBOR fixing, which is why the continued existence of LIBOR after 2021 remains questionable. The Swiss National Working Group has done valuable work to create the alternative reference rate, SARON.

Corporate

Law

Partial Abolition of Bearer Shares and Amendments to the Duty of Notification and Record-Keeping Obligation

Milestones

-

In force since 1 November 2019

Current status

Overview

The recommendations of the "Groupe d'action financière" (FATF) were incorporated into Swiss company law on 1 July 2015 (the so-called FATF Act). However, in the view of the Global Forum on Transparency and Exchange of Information for Tax Purposes (Global Forum), which assesses countries with regard to the exchange of information, the implementation of the transparency provisions of the FATF Act is not yet sufficient. The Federal Assembly has therefore decided on further measures, i.e. in company law (in particular the partial abolition of bearer shares), and adopted the Federal Act on the Implementation of the Recommendations of the Global Forum on Transparency and Exchange of Information for Tax Purposes (hereinafter referred as Global Forum Act) on 21 June 2019. As the referendum period has expired, the Federal Council has already set 1 November 2019 as the effective date.

Key changes

According to the act, bearer shares only remain permitted if the company has equity securities listed on a stock exchange or if the bearer shares are structured as intermediated securities. All companies that meet these requirements must have a corresponding note entered in the Commercial Register within 18 months of the law coming into force, i.e. by 30 April 2021. On 1 May 2021, impermissible bearer shares will be converted into registered shares. The Commercial Register Office records the amendments by law. It must also enter a note to the effect that the documents contain information that is inconsistent with the entry. Corporations/companies, whose shares have been converted by law must amend their articles of association when the next opportunity arises to do so.

After the conversion, the shareholders concerned must report to the company. The act also provides for a procedure to identify shareholders who have not complied with their duty to report to the company and whose shares have been converted. Within five years, these shareholders must request their entry in the share register by court order. Shares held by non-registered shareholders will become void five years after the entry into force of the act, i.e. on 1 November 2024. Nullified shares will be replaced by the company’s own shares.

The act also introduces criminal penalties for shareholders or companies that fail to report beneficial owners or to maintain the share register and the list of beneficial owners of shares. In addition, the act requires legal entities headquartered abroad with effective administration in Switzerland to keep a register of their owners at the effective place of administration.

Expert opinion

In Switzerland, almost 57'000 companies have still issued bearer shares and are potentially affected by this change in the law. For unlisted companies with bearer shares that are not structured as book-entry securities, it is advisable to convert these into registered shares as soon as possible.

If listed equity securities or bearer shares are available as intermediated securities, the corresponding entry can now be requested from the competent Commercial Register Office.

All companies should check whether the share register, the ordinary share register or the register of cooperative members and the register of beneficial owners comply with the legal requirements and whether the necessary supporting documents are kept correctly. Finally, access to the registers in Switzerland must be ensured at all times.

Overview

If a bank goes bankrupt, deposits of up to CHF 100,000 per client are treated as privileged under bankruptcy law. In case of an financial institute facing bankruptcy, the privileged deposits will be covered by the financial institute’s liquid assets outside of the ordinary collocation method as long as the claims can be settled. Otherwise, the difference up to CHF 100,000 per client will be funded by the deposit protection scheme.

The Federal Act on Banks and Savings Banks obliges banks, among other things, to finance the deposit protection through contributions levied by Esisuisse in the event of the bankruptcy of an institution.

Key changes

Disbursement period 1: Privileged deposits at Swiss branches should still be paid out immediately, and deposits at foreign branches should now be paid out as soon as effectively and legally possible from the liquid assets of the bankrupt institution.

Disbursement period 2: The transfer of secured deposits by Esisuisse to the liquidator has now to take place within 7 working days (instead of the previous 20 working days) since the FINMA notification. In addition, a new deadline is introduced under which the liquidator must pay deposits to depositors within 7 working days since receiving their payment instructions.

Safeguard measures: The safeguard measures should only trigger the deposit protection if they are ordered due to an imminent bankruptcy.

Financing method: Instead of permanently keeping liquid assets which equal a half of their respective contribution obligation, banks should now deposit easily marketable high-quality securities or Swiss francs in cash with a third-party custodian to the same extent.

Preparatory measures: In order to speed up payments to depositors, banks are required to carry out certain preparatory tasks with regard to their data situation, processes and infrastructure. The creation of a list of depositors ("master file") is central which records all depositors with secured deposits. A transition period of 5 years is intended.

Maximum obligation: The upper system limit for deposit protection is now 1.6 percent of deposits secured, but at least six billion Swiss francs.

Expert opinion

The proposed changes are likely to strengthen confidence in the Swiss financial centre and at the same time improve its stability. The new, relatively short deadlines for disbursement to depositors are intended, among other things, to avoid bank-runs at third-party banks and financial bottlenecks of depositors. The adjustment of the maximum obligation to 1.6% ensures that the payment obligations are linked to the amount of secured deposits.

However, banks will also have to make a considerable amount of effort as a result of the planned changes. For example, the requirement to hold liquid securities or cash deposits with third-party institutions will lead to some adjustments. In addition, banks should analyse the requirements for preparatory actions with regard to data quality, processes and infrastructure at an early stage - despite the transition period - and begin with implementation planning.

Banking Act

Deposit Protection

Milestones

- 8 March 2019: The Federal Council opens consultation process on partial amendment of the Banking Act

- 14 June 2019: End of the consultation process

- The dispatch of the Federal Council on the amendment of the Banking Act is expected to be adopted in spring 2020

Current status

Changes in Bank Accounting and Reporting

Provisions for Loan Default Risks

Milestones

- The hearing was held until 18 June 2019

- 1 January 2020: Revised accounting ordinance is expected to come into force

- Transitional periods should not be extended beyond 31 December 2026

Current status

Overview

The Swiss Financial Market Supervisory Authority (FINMA) is restructuring the accounting regulations for banks. It adapts the method for determining value adjustments for credit risks by introducing new approaches for expected losses or inherent default risks. To this end, it replaces the previous circular on banks‘ accounting/reporting standards with a principle-based ordinance and a streamlined circular.

Key changes

The FINMA Accounting Ordinance contains the fundamental provisions on valuation and recording. The Circular describes FINMA’s practice on accounting/reporting and disclosure issues. FINMA issues these standards as the authority defining the accounting/reporting standards for banks in Switzerland. The Ordinance and the Circular will enter into force on 1 January 2020 with a transitional period of up to six years exists.

FINMA is altering the approach for the creation of value adjustments for the default risks of non-impaired receivables in order to address and mitigate weaknesses, particularly, the risk of a procyclical effect due to value adjustments being created too late. This issue was also addressed by the international accounting/reporting standards: IFRS has applied the new approach since 2018 whereas the US GAAP will introduce it in 2020. By comparison, the new approaches for the creation of value adjustments for default risks according to Swiss standards are more principle-based and much simpler.

Furthermore, the new approach for the creation of value adjustments for default risks are proportional to the size of the bank: Only system-relevant banks have to model the expected losses in their portfolios of loans in detail. The participants in the hearing particularly welcomed this proportionality and the methodological scope for action granted to them. At the request of the hearing participants, FINMA incorporated individual elements of the explanatory report into the ordinance. However, FINMA did not include any further definitions in connection with the new valuation allowances, as this would restrict the deliberately granted freedom of method and contradict the principle-based approach.

Expert opinion

The adjustment effort in connection with value adjustments for default risks is determined in particular by the FINMA supervisory category in accordance with the proportionality principle. The need for action can be summarised as follows:

All banks

- Revision of the valuation guidelines by 31 December 2020

- Determination of the maximum period for creating value adjustments for expected losses and inherent risks (maximum linear over 6 years).

Banks in categories 4 and 5, as well as medium-sized banks (category 3) which do not operate primarily in the interest rate business

- Analysis of value adjustments for latent risks and decision on the use of resulting annual surplus as for 2020 (inherent risks or release / creation of hidden reserves)

Overview

The Swiss fund market is of great importance for the economy as a whole and is also internationally known as an asset management and distribution hub, but is less well positioned as a producer. This is mainly due to the fact that foreign legislations have more favourable framework conditions for alternative and innovative fund products. The EU states have already introduced fund categories that do not require prior approval from the respective supervisory authority.

With the partial amendment of the Collective Investment Schemes Act (CISA), the Federal Council intends to promote the innovation and competitiveness of the Swiss fund market.

Key changes

The so-called "Limited Qualified Investor Fund" (L-QIF) is intended to offer a Swiss alternative to similar foreign products. From a taxation standpoint, the L-QIF is treated like a fund without being subject to FINMA approval. For the L-QIF, the regulator has abandoned its previous dual supervision of institution and product, which in fact enables deregulation. Nevertheless, the L-QIF remains embedded in the regulatory framework as the management of the fund has to be transferred to an authorised fund management company.

The L-QIF may be issued without a prospectus and is generally not subject to any external restrictions with respect to investment instruments and risk diversification. This gives market participants the opportunity to set up a fund product much more quickly and cost-effectively.

The provisions of the CISA also in principle apply to an L-QIF - with the exception of the provisions on licensing, approval and supervision by FINMA. Thus, an L-QIF can be established in one of the four legal forms provided for in the CISA (contractual investment fund, SICAV, KmGK or SICAF).

The lack of a licensing and approval requirement does not mean that the investors of an L-QIF remain without protection. For example, the L-QIF is only available to qualified investors under the CISA, such as banks, insurance companies and pension funds, who have been previously approved and supervised by FINMA. The latter are already allowed to invest in unregulated foreign funds.

The opinions expressed during the consultation process were largely very positive. In some cases, even more extensive deregulation was desired, especially with regard to the obligation to transfer the management of the fund to an authorised fund management company.

Expert opinion

We welcome Switzerland’s deregulation for such fund products and hope that innovative Swiss market participants will take advantage of the opportunity to create new products and attract substantial assets.

The simpler and more cost-effective launch is a positive development. Even more valuable though is the freedom with regard to freely selectable investments and risk distribution requirements. These must of course be defined and adhered to for the respective L-QIF, but are not subject to any legal restrictions.

In recent years, Switzerland has positioned itself very well globally as an innovation driver with new financial market participants and investment opportunities. The L-QIF offers great potential in this respect.

Collective Investment Schemes

Implementation of New Fund Categories

Milestones

- 26 June 2019: The Federal Council opened the consultation procedure; the consultation process lasted until October 17, 2019

- Q3/2020: Expected entry into force

Current status

Pro-portionality in Supervision and Regulation as well as Small Banks Regime

Amendments to the Capital Adequacy Ordinance (CAO) and FINMA Circulars

Milestones

- October 2017: Small Bank symposium and following in 2018: Workshops with SBA, banks, SIF, SNB, EXPERTsuisse

- July 2018: Start of the small banks regime pilot phase.

- April - July 2019: Amended CAO for consultation and various adapted FINMA circulars

- 1 January 2020: Entry into force of the amendments in CAO and adapted FINMA circulars

Current status

Overview

Both the financial market regulation and the risk-oriented supervision of FINMA follow a certain proportionality principle. This means that regulation and supervision take into consideration the different sizes, business models and risks of the individual institutions. In addition to the existing FINMA practice of risk-oriented supervision, small, particularly liquid and well-capitalised banks can be relieved from unnecessary administrative burden through regulatory relief and simplifications. In return, these institutions are obliged to hold additional equity capital and liquidity and may not be exposed to increased risks in the area of conduct as well as credit risks.

Key changes

Most of the reliefs under the proportionality principle are generally granted automatically to small institutions with a few exceptions. One exception is the reduced audit frequency according to FINMA Circular 13/3 «Auditing». The Board of Directors can apply to FINMA for extended audit cycles for the supervisory audit (instead of once every two years (Cat.4) or those institutions in Category 5 once every three years).

In order to benefit from the alleviations of the small bank regime, the financial institution in Category 4 or 5 must first fulfil a number of criteria:

- A simplified leverage ratio in excess of 8%

- An average liquidity coverage ratio of over 110% over the past 12 months

- A refinancing rate of over 100% an no increased risks

FINMA may also reject the application for simplification if supervisory measures or procedures relating to rules of conduct (e.g. AMLA, FIDLEG) have been initiated. FINMA may also reject the application if an institution is managing its interest rate risks inadequately or is exposed excessively to interest rate risks.

The simplification of the small banks regime include in particular:

- Elimination of capital adequacy requirements, including the calculation of risk-weighted assets, as well as the eliminiation of capital buffers and sectoral application of the countercyclical capital buffer.

- No need to calcute or comply with NSFR (liquidity).

- Qualitative simplifiaction in FINMA Circulars (e.g. requirements for handling electronic client data, disclosure obligations; risk control, outsourcing and internal auditing).

Expert opinion

In principle, risk-oriented financial market regulation and supervision are to be encouraged. However, the system of proportionality principle and small bank regimes appears to be relatively complicated to apply. It remains to be seen whether the increased frequency of audits will really lead to lower costs or simply to a shift in the focus and whether the quality of the audit will not suffer due to the longer audit cycles.

Overview

On 1 June 2018, the Federal Council opened the consultation on the amendment of the Anti Money Laundering Act (AMLA ). The aim of the consultation was to implement the most important recommendations from the country report of the Financial Action Task Force (FATF) as part of the fourth country assessment of Switzerland. The planned changes in the AMLA primarily address the weaknesses raised by the FATF (e.g. lack of subordination of lawyers, notaries and trustees to the AMLA in connection with certain non financial activities, too low number of suspicious activity reports in relation to the importance of the Swiss financial center, etc.). On 26 June 2019, the Federal Council adopted the dispatch on the amendment of the AMLA. On the basis of the results of the consultation procedure, the Federal Council adjusted two measures in relation to the consultation draft in the area of the new AMLA subordination of advisors. At the same time, the Federal Council included a new measure in the draft within the scope of reporting. The AMLA is expected to enter into force at the beginning of 2021.

Key changes

New due diligence requirements for advisers: The due diligence and audit duties for advisers should only apply to commercial services in connection with trusts and domiciliary companies (and no longer to all other companies). In addition, the duty to report to the Money Laundering Reporting Office Switzerland (MROS) is to be introduced. However, this only applies if a financial transaction is carried out for the client during the activity and the data to be reported are not covered by professional confidentiality.

Verification of the information on the beneficial owner: The obligation of the financial intermediaries to verify information about the beneficial owner is now explicitly listed as an obligation. The financial intermediary must apply the necessary diligence according to the circumstances to find out the beneficial owner’s identity.

Constant updating of client data: The client data must be periodically checked for up-to-dateness and must be updated if necessary. There is no limitation to the identification of the contracting party and establishing the identity of beneficial owners. The new explicit obligation may also include a more general review of the client profile, such as the nature and purpose of the business relationship, where such information is relevant to the risk classification or monitoring of the business relationship. The duty to periodically check the validity of the client data applies to all business relationships irrespective of the risk. However, the frequency, the scope, the type of review and the constant updating of client data may depend on a risk-based approach.

MROS: Contrary to the original plan of the Federal Council, the duty to report under the AMLA and the right to report under the Criminal Code are to be retained. The term "justified suspicion" is to be explained on the basis of the corresponding jurisprudence of the Federal Supreme Court in the Anti-Money Laundering Ordinance (AMLO). The right of the financial intermediary to terminate a business relationship, which was the subject of a suspicion report, is also proposed as a new measure to enshrine in the AMLA (if the financial intermediary has not received any feedback from the MROS after 40 days have elapsed). This provision is to apply to reports based on duty to report and to the right to report.

Expert opinion

A clarification or specification of the requirements for the "justified suspicion" or a clear definition of this term in the AMLO is absolutely necessary. A clarification/specification is also necessary on the basis of the principle of legality for the protection of financial intermediaries, since both intentional and negligent breaches of the duty to report are still punishable by law (Art. 37 AMLA). According to the Federal Council’s dispatch, the clarification of the concept of "justified suspicion" should take account of jurisprudence of the Federal Supreme Court.

Additionally, the right to report should "in no case" represent competition to the duty to report, or it should be ruled out that a case falls simultaneously under the right to report and the duty to report. It remains to be seen whether, in view of the fact that every potential suspected case is unique and requires an individual assessment, this "black-and-white" approach will be so easy to implement in practice.

AMLA

Revision of the Anti-Money Laundering Act

Milestones

- June – September 2018: Consultation on the changes in the AMLA

- 26 July 2019: Publication of dispatch on the amendment of the Anti-Money Laundering Act (AMLA)

- 1 January 2021: Expected entry into force of the revised AMLA

Current status

AMLO-FINMA

Revision of the FINMA Anti Money Laundering Ordinance

Milestones

- 18 July 2018: Publication of partially revised AMLO-FINMA

- 1 January 2020: The AMLO-FINMA will enter into force together with the revised Agreement on the Swiss Banks' Code of Conduct with Regard to Due Diligence (CDB 20)

Current status

Overview

In connection with the implementation of the recommendations from the FATF country examination, the AMLO-FINMA will also be revised. The partial revision is intended to implement those adjustments that are necessary to enable Switzerland to leave the FATF's "enhanced follow-up" process. In addition, findings from FINMA's supervisory and enforcement practices will be incorporated into the partial revision.

Key changes

Clarifications with domiciliary companies: The revised AMLO-FINMA explicitly requires the clarification and recording of the reasons for the use of domiciliary companies.

High-risk business relationships and transactions: When identifying business relationships or transactions involving increased risks, financial intermediaries must take into account both residency and payments from or to a country regarded by the FATF as "high risk" or "non-cooperative".

The complexity of the structures - in particular through the use of several domiciliary companies or one domiciliary company with fiduciary shareholders, in a non-transparent jurisdiction, without comprehensible reason or for the purpose of short-term placement of assets - are also regarded as criteria for increased risks.

Financial intermediaries must individually determine on the basis of a risk analysis whether the risk criteria specified in the Ordinance are relevant to their business activities. The relevant criteria must then be specified in internal directives and taken into account when determining business relationships with increased risks.

Branches and group companies abroad: Swiss financial intermediaries with branches and group companies abroad are particularly affected. According to AMLO-FINMA, a risk analysis must be prepared on a consolidated basis and standardised reporting (qualitative and quantitative information) must be carried out.

Decision-making authority for reports: It is explicitly stated that the highest management body (management) must decide on the exercise of the duty of report pursuant to Article 9 of AMLA or the right to report pursuant to Article 305ter para. 2 of the Swiss Criminal Code. This decision-making authority may be delegated to one or more members of the management who are not directly responsible for the management of business relationships, to the Money Laundering Unit or to a largely independent body.

Expert opinion

According to FINMA's explanatory report of 4 September 2017 on the partial revision of AMLO-FINMA, the obligation to clarify the reasons for the use of domiciliary companies in Art. 9a of AMLO-FINMA is not new, as financial intermediaries are already obliged to identify the purpose of the business relationship requested by the contracting party. However, the newly created duty to clarify sets an earlier stage and includes not only the type and purpose of the business relationship between the domiciliary company and the financial intermediary, but also why a client (or beneficial owner) uses a domiciliary company to invest his assets in the first place. Financial intermediaries will therefore have to clarify in greater detail in future whether the use of a domiciliary company pursues a legitimate and legal purpose, particularly with regard to tax declaration obligations and taking into account the predicate offence of a qualified tax offence.

Overview

The revised Agreement on the Swiss Banks' Code of Conduct with regard to Due Diligence (CDB 20) was issued by the Swiss Bankers Association (SBA) and will enter into force in parallel to the revised AMLO-FINMA on 1 January 2020. Stricter self regulation is an important element in the fight against money laundering and terrorist financing. The revised Agreement also addresses the need for improvement in combating money laundering identified by the Financial Action Task Force (FATF).

Key changes

Duty to report: An account without complete documentation and information on the contracting party, on the beneficial owner or on the control holder must be blocked after 30 days (instead of the previous 90 days) for all entries and withdrawals. The business relationship must be terminated in any case if the missing information or documents cannot be completed.

Lowering the threshold for cash transactions: The threshold for identifiying the contracting partner in cash transactions will be lowered from CHF 25,000 to CHF 15,000. The financial intermediary is obliged to identify the contracting party at all times when executing transactions involving trading in securities, currencies and precious metals as well as other commodities.

Video and online identification: With the inclusion of FINMA Circular 2016/07 on video and online identification in CDB 20, the identification in the case of a personal interview is treated in the same way as video identification and the identification in the case of a business relationship by correspondence is treated in the same way as online identification.

Abbreviated process by the supervisory board: The rules for the abbreviated process for simple cases as part of the self indictment disclosure were specified. The audit companies are now more closely involved in the process as the bank submits the complete files of the case as well as the report to an audit company for the purpose of self indictment. The audit company's report describes the facts of the case and names the relevant provisions of the Code of Conduct as a minimum.

Adjustments to the forms: There are also clarifications and simplifications for forms A, K, I, S and T.

Expert opinion

The consequences of the current changes for the financial intermediaries affected should not be underestimated, although the core content of the previous CDB remains unchanged.

Due to the shortened deadline for the provision of the documents and other information about the contracting party, the beneficial owner and/or the control holder, the onboarding processes must be adapted with stringent controls regarding the compliance with the deadline as well as the account blocking for entries and withdrawals and the termination of business relationships.

Furthermore, the financial intermediaries affected must train their staff with regard to lowering the threshold for cash transactions and adapt the underlying processes and controls (e.g. forms, transaction monitoring, compliance controls).

CDB 20

Revision of the Agreement on the Swiss Banks' Code of Conduct with regard to Due Diligence

Milestones

- 4 April 2019: The SBA’s commentary on CDB 20 was published on 4 April 2019; the guideline is available here

- 1 January 2020: CDB 20 is closely related to the AMLO-FINMA and it is therefore appropriate that both will enter into force on 1 January 2020

Current status

MiFID II

Markets in Financial Instruments Directive

Milestones

- 3 January 2018: MiFID II enters into force

- Since July 2018: After a transitional period of six months, trading without LEI (Legal Entity Identifier) is no longer possible

Current status

Overview

After a long lead time, the revised European Markets in Financial Instruments Directive (MiFID II) entered into force on 3 January 2018. The core element of this revision particularly is the strengthening oft he provisions aimed at protecting investors. Various current studies on the implementation status among European financial service providers show that MiFID II requirements have been well implemented overall. No corresponding studies could be found for Swiss financial service providers with European customers, but we assume that there are major differences between the financial institutions with regard to the implementation status of MiFID II. Since the Directive came into force, the ESMA (European Securities and Markets Authority) has published various amendments to the Q&As in connection with the customer protection provisions of MiFID II and MiFIR, which are used to interpret the provisions.

Key changes

- Extension of the information duties in connection with costs incurred

- Introduction of the distinction between independent and non-independent investment advice

- Requirements for the provision of independent investment advice

- Prohibition of accepting commissions (e.g. retrocessions) for asset management and independent investment advice

- Introduction of monitoring duties in connection with the distribution of financial instruments (product governance)

- Obligation to record telephone conversations in connection with client orders

- Obligation to submit a suitability report for investment advice

- Loss threshold reporting for asset management mandates from a loss of 10% of the total portfolio

- Quarterly preparation of client reports (or monthly for portfolios with leverage)

Updates since our Regulatory Radar 1st Edition 2019:

- Specifications in connection with cost information for asset management mandates

- Clarification of the interplay between the annual ex-post cost information ant the periodic reports

- Regulation in the event of conflicting product intervention rules in the Member State and the country in which the investment sercice is provided

Expert opinion

Due to the consumer court of jurisdiction under the Lugano Convention, the MiFID II customer protection provisions may also be relevant for Swiss financial service providers. We therefore recommend conducting a risk analysis along the following questions:

- Which services do I currently provide for my EU clients?

- Which services and EU markets have strategic relevance for my company?

- What is the gap between the target status according to MiFID II and my current status of service provision?

- How high is the risk of lawsuits from EU customers?

- What are MiFID II “quick wins" and which duties must also be fulfilled under the FinSA?

Overview

The Financial Services Act - together with the Financial Institutions Act (FinIA) - will enter into force on 1 January 2020. The purpose of FinSA is the cross sector regulation of financial products and financial services as well as their distribution («same rules for same business»). FinSA also intends to improve and standardise client protection and strengthen the reputation and competitiveness of the Swiss financial center.

The law is based on the European MiFID II directive, but is clearly more sector friendly on certain points (e.g. regulations on retrocessions, assessment of suitability etc.). In order to give financial service providers sufficient time to implement the new regulation, a two year transitional period is planned for the fulfilment of most FinSA duties.

Key changes

- Client segmentation (retail clients, professional clients, institutional clients) including options for opting-in/opting-out.

- Assurance of sufficient knowledge of the FinSA Code of Conduct and the necessary expertise for Relationship Managers.

- Comprehensive information and documentation duties towards clients in connection with the onboarding and the provision of the service.

- Provision of a key information document (KID) for investment advice (and execution only) for retail clients. In addition to the type and characteristics of the financial instrument, this KID also contains risk and return profile, tradability, minimum holding period and corresponding costs of the financial instrument.

- Carrying out an appropriateness test (for transaction-related investment advice) and a suitability test (for portfolio-related investment advice and portfolio management)

- Obligation to register investment advisers in the register of advisers. This applies to all advisers who do not require a licence, recognition, authorisation or registration under the Financial Market Supervision Act (FINMASA).

- Affiliation to a professional liability insurance or corresponding securities and affiliation to an Ombudsman.

Expert opinion

The provisions of FinSA will enter into force on 1 January 2020 (a transitional period of two years will apply to various FinSA duties). This poses some potential challenges for Swiss financial service providers, though many of the provisions are already known from the Code of Conduct. In contrast to its European equivalent MiFID II, the FinSA leaves considerably greater scope for entrepreneurial flexibility.

It can be assumed that the FinSA/FinIA will not cause the considerable upheavals once feared in the financial sector. Nevertheless, it is advisable to carefully analyse the new requirements and to make necessary adjustments, e.g. with regard to the organisational setup, client information policy or contractual framework.

FinSA / FinSO

Financial Services Act /

Financial Services Ordinance

Milestones

- 6 November 2019: Publication of FinSO

- January 2020: Entry into force FinSA/FinS0 (a two year transitional period is planned for the fulfilment of most FinSA duties)

- December 2021: Expiry of the most transitional periods for the implementation of FinSA

Current status

FinIA / FinIO

Financial Institution Act /

Financial Institutions Ordinance

Milestones

- 6 November 2019: Publication of FinIO

- January 2020: Entry into force of FinIA

- 1st quarter 2020: Start of consultation on amendments to the existing FINMA ordinances

- 4th quarter 2020: Adoption of the amended FINMA ordinances

- December 2022: Expiry of the deadline for fulfilling the authorisation requirements and submission of the licence application

Current status

Overview

FinIA and FinIO unify the licensing rules for asset managers, collective asset managers, fund management companies and investment firms by introducing prudential and thus comprehensive supervision for all service providers. The licensing cascade for asset managers and trustees (first stage of the cascade) stipulates a significantly lower supervisory intensity and also lower regulatory requirements compared to the higher stages (e.g. banks and investment firms).

The final version of FinIO was published on 6 November 2019 at the same time as FinSO. FinIA and FinIO will enter into force together with FinSA and FinSO on 1 January 2020.

Key changes

Authorisation requirements and supervisory regime

- From the entry into force of the FinIA, asset managers and trust companies will also be prudentially supervised. The supervision is carried out using a mixed model: FINMA is responsible for licensing and enforcement, while the annual supervision is carried out by newly formed supervisory organisations.

- Asset managers and trust companies that are now subject to an authorisation requirement must report to the supervisory authority within six months of the FinIA coming into force and submit the corresponding licence application within two years.

- Only investment advisers are exempt from the authorisation requirement, but they must be entered in a register of advisers.

Organisation, Corporate Governance and Risk Management

- The financial institution must establish appropriate corporate governance rules.

- The persons responsible for the administration and management of the financial institution are subject to proper business conduct requirements.

- The financial institution identifies and monitors its risks and ensures an effective internal control system.

- Persons performing risk management or internal control duties shall not be involved in the activities they supervise (exceptions for risk-free micro-setups).

Requirements for own funds and financial guarantees: Financial service providers must comply with minimum capital requirements, adequate own funds and financial guarantees or conclude a professional liability insurance.

Expert opinion

FinIA will not - contrary to initial fears - lead to a radical "consolidation" among external asset management companies of small size. However, it is important to take action at an early stage in order to be well prepared both from an organizational point of view (e.g. by implementing an internal control system and an independent compliance function) and with regard to newly established authorisation requirements, minimum capital requirements etc.

Overview

The Federal Council's report on the legal framework for blockchain and distributed ledger technology (DLT) of December 14, 2018 demonstrated that while the Swiss legislative framework is in general already well adapted to the new technologies, there is still a need for adjustments in some areas.

Subsequently, in March 2019, the Federal Council sent a series of amendment to existing laws for consultation. During its meeting on November 27, 2019, the Federal Council adopted the dispatch on the “Federal Act on the Adaptation of Federal Law to Developments in distributed ledger technology”. These include, in particular, amendments in the Code of Obligations and securities law, debt enforcement and bankruptcy (“DEBA"), Banking Act (“BA"), Anti Money Laundering Act (“AMLA”) and Financial Market Infrastructure Act (“FMIA").

Key changes

Securities law: In addition to the existing categories of securities, uncertificated securities and book-entry securities, a new category of so-called DLT-registered uncertificated securities will be introduced. Tokens that represent a legal position (claim, membership) are to fall into this category. DLT-registered uncertificated securities are to be created and transferred by entry in manipulation-resistant electronic registers.

DEBA: Within the DEBA, it is intended to introduce the segregation of cryptobased assets due to bankruptcy, provided that these are either individually assigned to a third party or are assigned to a community asset and that it is clear which share of the community assets the third party is entitled to. In addition, in the sense of segregation, access to data in the custody of the bankrupt's estate is intended.

BA: The segregation of cryptobased assets in the event of bankruptcy has an impact on possible banking licence requirements, as segregatable assets are not considered deposits. Nevertheless, due to reputation reasons, the Federal Council has planned to subject the collective custody of certain cryptobased assets to the banking licence referred to as "Fintech" or "BA 1b“– which will be further defined by the Federal Council, as long as that they are not mixed with bank assets and no lending business is conducted (otherwise a banking licence according to Art. 1a BA may be required).

FMIA: The FMIA provides for the creation of a new authorization category for "DLT trading facilities" to trade with DLT securities multilaterally (register value rights, but not payment tokens/utility tokens) according to non-discretionary rules.

AMLA: The DLT trading facilities will be defined as financial intermediaries and thus are subject to the AMLA obligations.

Expert opinion

The creation of so-called DLT-registered uncertificated securities increases the legal certainty regarding the issuance and transferability of cryptobased assets. The segregation of cryptobased assets is also suitable for promoting the acceptance and dissemination of cryptobased assets. The new “DLT trading facilities” for private customers will enable access to multilateral DLT trading facilities. Trading platforms should therefore review their activities with regard to the definition of the “DLT trading facilities” and the associated FMIA licensing requirements.

Custodians of cryptobased assets should carefully monitor further developments, in particular the list of crypto values to be published by the Federal Council, and if necessary investigate whether their activities require a licence under the Banking Act.

It will be interesting to see which additional adjustments are planned in the area of insurance and collective investment schemes.

Fintech (1/2)

Federal Act on the Adaptation of Federal Law to Developments in Distributed Ledger Technology

Milestones

- 25 June 2014: Federal Council’s report on virtual currency

- 14 December 2018: Second report on the legal framework for blockchain and distributed ledger technology (DLT)

- 22 March 2019: Consultation on improving the framework conditions for DLT/blockchain

- 27 November 2019: Dispatch on the “Federal Act on the Adaptation of Federal Law to Developments in DLT

Current status

Fintech (2/2)

Accounting Treatment and Regulatory Requirements for Payment Tokens

Milestones

- October 2018 / January 2019: FINMA guidlines concerning payment tokens / accounting treatment and the resulting regulatory requirements

- September 2019: Joint paper of EXPERTsuisse and Crypto Valley Association (CVA)

Current status

Overview

At the end of 2018 and the beginning of 2019, FINMA reached out to the audit firms and a number of institutions concerned, expressing its views for the first time on the accounting treatment and the resulting supervisory requirements in connection with payment tokens.

In addition, EXPERTsuisse and the Crypto Valley Association (CVA) are in close cooperation on issues of accounting according to the Code of Obligations for Bitcoins and ICOs. As a result, a joint paper was presented on the questions in this regard.

Key changes

The accounting obligation for payment tokens is essentially determined by whether, in the event of bankruptcy of a bank, they can be separated out in favour of the entitled customers or not. The separability is assumed to be given if the credit balances in payment tokens are kept separately per customer on the blockchain and can be assigned to the individual customer at any time.

To the extent that payment tokens have to be accounted due to lack of separability, the accounting treatment is as follows:

- Assets: The payment tokens held on the assets side for customers are treated in the same way as physical precious metal holdings and are valued and balanced at fair value under the item "Financial assets". Payment tokens held for own account (own positions on the assets side of the balance sheet) are shown in the balance sheet under "trading transactions" if the general conditions for this are fulfilled. Otherwise, they are treated as financial assets at the lower of cost or market.

- Liabilities: Liabilities-side customer positions with payment tokens are measured and recognised at fair value under liabilities from customer deposits. In order to avoid incongruity in the income statement, value adjustments are booked under "Other ordinary expenses/income".

- Equity capital: Positions in payment tokens are assigned a blanket risk weight of 800% to cover market or credit/counterparty risks, irrespective of whether the positions are held in the banking or trading book.

- Liquidation requirements: In order to cover a possible net outflow of funds, banks must at all times maintain sufficient high-quality HQLA, which is to be expected in a stress scenario with a 30-day horizon.

Expert opinion

The risk weighting of 800% for backing market and credit/counterparty risks appears to be very high. Nevertheless, it is to be welcomed that FINMA is creating clarity with this regulation. According to a survey conducted by the Basel Committee on Banking Supervision among its member states, this value currently corresponds to an average international value. We expect that the high risk weight will be reduced due to international competition between locations, and when a broad market adoption and technological developments progress.

Overview

Since the new EU data protection basic regulation ("GDPR") is applicable, a more stringent data protection applies in European Economic Area (EU incl. EEA countries) than in Switzerland. The first fines in the EU/EEA based on the GDPR have already been imposed.

In the meantime, most of the Swiss financial service providers have at least considered the basic principles of GDPR and have laid down certain minimum requirements in writing in directives and/or process descriptions. It is considered to be certain that the documentation- and process-focused GDPR regulations are mapped analogously in the totally revised CH-DSG and that financial service providers in Switzerland fall under the new European data protection regulations anyway due to broad geographical scope of the GDPR.

Key changes

- The total revision of the Federal Data Protection Act ("DPA") will take place in two stages. With a focus on the criminal law area of personal data, the Federal Council put the data protection provisions for Schengen cooperation in criminal matters into force on 1 March 2019.

- The draft of the other part of the totally revised DPA is currently being discussed by Parliament and in particular aims to improve the protection of our personal data and the position of citizens and to adapt data protection to technological and international legal developments. The adaptation of the legislation to the European law is intended to ensure that cross-border data transmission between Switzerland and the EU/EEA states remains possible without additional obstacles. However, Switzerland does not introduce any rules that are stricter than necessary.

- The draft is risk-based, technology-neutral and enables to act in the important European market. For example, in the case of profiling, explicit consent should only be required if profiling is associated with a high risk for the personality or fundamental rights of the person concerned. Furthermore, the appointment of an internal data protection officer should be voluntary and strengthen the possibility of self-regulation.

- Swiss companies are affected by the GDPR if they "obviously intend" to offer their services to persons concerned in an EU/EEA member state. For example, when using a language, currency or telephone number with an international prefix used in the EU/EEA Member State. But the use of a top-level domain from another EU/EEA country for distribution from Switzerland to the EU would also be such an indication.

- First judgements from the EU/EEA show that data protection authorities and data subjects are filing claims for damages from the data processor in accordance with the GDPR and that courts agree with these claims.

Expert opinion

The GDPR shapes the revision of the Swiss Data Protection Act. If Swiss financial service providers are not already impacted by the GDPR, the same requirements must be met under the revised DPA with few exceptions.

Therefore, the current state should be analysed in order to know, where, by whom, which data, for what purpose and how long the data will be processed. This process must be described and all information must be summarized in a central register. This enables proof of lawful processing and the acquisition of any gaps.

Data Protection

GDPR and FADP

Milestones

- Since 25 May 2018: The GDPR is directly applicable (if necessary also in Switzerland)

- Switzerland has approximately two years to revise the FADP and to restore the equivalence of the regulation of the controversial points (e.g. EU sanction mechanism, definition of particularly sensitive data) with the GDPR

- The revised FADP is expected to come into force in 2021

Current status

Self-Regulation

Mortgage Financing

Milestones

- Both revised guidelines enter into force on 1 January 2020

- A transitional period of six months (until 30 June 2020) is provided for any adjustments to technical systems

Current status

Overview

The Swiss Financial Market Supervisory Authority FINMA recognises the amended self-regulation of the banking sector on mortgage financing as a minimum standard. The changes will tighten the requirements regarding the loan-to-value ratio and amortisation of mortgage loans for investment properties. Owner-occupied residential properties are not affected by the adjustments. The revised guidelines will enter into force on 1 January 2020.

Key changes

The self-regulation comprises the guidelines on minimum requirements for mortgage financing and the guidelines on the assessment, evaluation and settlement of mortgage-backed loans. The partially revised guidelines contain the following changes:

- In the case of mortgage financing of investment properties, the minimum down payment will increase to 25% of the loan-to-value ratio (instead of 10%). The requirement to finance any difference between the higher acquisition price and the lower loan-to-value entirely from the borrower's own funds (lowest value principle) remains unchanged.

- It should be noted that investment properties are properties held for investment purposes and leased to third parties (not owner-occupied residential properties) - irrespective of the legal form of the debtor and the amount of the loan-to-value ratio.

- The tightened rules only apply to new borrowers and to loan increases, but not to extensions.

- The mortgage of investment properties must be amortised to two-thirds of the loan-to-value ratio of the property within a maximum of 10 years (not 15 years).

- Owner-occupied residential properties are not affected by the adjustments. The minimum down payments from own funds remains unchanged at 10% (excl. assets from the 2nd pillar).

- The buy-to-let segment, which is essential in Switzerland, is also not affected. Buy-to-let properties are properties that are bought by private individuals but not occupied by them (condominiums and single-family homes). FINMA recommends that banks voluntarily apply the new standards to these properties as well.

Expert opinion

The tightened minimum requirements via the self-regulatory method is to be welcomed. It remains to be seen in the longer term whether the measures, despite their limitations, will be sufficient to sustainably prevent the real estate market from overheating.

There is a short-term urgency with the adjustments to internal directives and processes, which must be tackled before the end of the year.

Overview

The UK’s Financial Conduct Authority (FCA), which is responsible for monitoring the LIBOR reference rate, has announced on 27 July 2017 its intention not to require banks contributing to the calculation of LIBOR to participate in the LIBOR benchmark interest rate from 2021 onwards. The FCA bases its decision on the fact that LIBOR is based on inadequately executed transactions and is also susceptible to manipulation. As an alternative to LIBOR, reference rates have been and are being developed worldwide at the national level. The starting value for the Swiss franc rate curve and thus a replacement for CHF LIBOR is SARON.

Key changes

The Swiss Average Rate Overnight (SARON) reflects the conditions for overnight money transactions in the secured CHF money market and is administered by SIX Swiss Exchange.

The SARON is a volume-weighted average based on completed transactions and binding quotes in the order book of the SIX Swiss Exchange electronic trading platform. Outliers are adjusted by applying a quote filter. The calculation methode was developed in cooperation with the SNB and is publicly accessible and transparent.

The SARON is calculated immediately after the close of trading (18:00), with additional fixings during the trading day at 12:00 and 16:00.

The SARON has a clear governance structure and meets the requirements of international benchmark standards. At the beginning of 2017, the SIX also established the SRR Index Commission, which regularly reviews all aspects of SARON.

Based on these properties, the National Working Group recommended SARON as an alternative to CHF LIBOR in October 2017.

The operational challenges of the changeover are manifold. Examples include:

- Designing new products

- Identification of internal and external IT dependencies

- Adaptation of collateral management

- Adaptation of back-office processes

- Adaptation of valvation & risk models

- Adaptation of new and old contracts

- Internal and external communication

- Etc.

Expert opinion

The end of LIBOR is foreseeable. The SARON seems to be a representative and robust substitute for CHF LIBOR.

The first step in the transition from LIBOR to SARON should be to determine as quickly as possible to what extent you are actually affected. Which products, values and processes depend on LIBOR? It is also important to address the operational challenges in time and to make a conscious decision as to whether it might you need to act or can wait for the moment.

SARON

A Substitute for LIBOR?

Milestones

- 27 July 2017: Announcement of FCA that it no longer intends to support the LIBOR benchmark interest rate from 2021 onwards

- 5 October 2017: Recommendation of SARON as reference rate

- Possible scenario after 2021: no more LIBOR pricing available

Current status